Building a Growth Engine for Experience Travel

For most of the last decade, multi-day operators have evaluated travel tech by one measure: how much manual work it eliminates. That framing is now outdated.

The operators winning market share - names like Railbookers and Tauck - are using their tech stack as commercial infrastructure instead of operational plumbing. They are driving conversion, lifting revenue per booking, and expanding into new channels.

The opportunity is significant. According to the United States Tour Operators Association (USTOA), member companies projected $24.4 billion in annual revenue and to serve 8.4 million travelers in 2024, with operators projecting more than 8% sales growth year over year. That momentum has held: in USTOA's most recent forecast survey, two-thirds (68%) of tour operators reported higher sales in 2025 than in 2024, and half of those saw gains of 10% or more — well ahead of the pace of the broader travel industry.

Why "Efficiency" Stopped Being Enough

Multi-day travel was never simple. A single booking can involve six suppliers, four currencies, three transfers, two countries, and a customer who expects to text their agent on a Sunday. For years, the technology conversation focused on managing that complexity - cutting admin time, eliminating duplicate data entry, getting itineraries out the door faster.

Those problems still exist. But solving them no longer creates a competitive moat.

Today's operators are losing deals for different reasons.

They are losing them because a competitor quoted faster. Because a traveler bounced from a clunky payment page. Because the upsell logic on a luxury safari was generic instead of personalized. Because the operator could not launch a new product line fast enough to meet demand.

The deeper issue is how technology is framed internally.

Most operators still treat software decisions like procurement exercises with requirements lists, feature parity, and replacement projects. The conversation stays in operations; it rarely reaches the commercial leadership team.

But that framing has a cost.

Arival's research has found that only 53% of multi-day tour operators use a dedicated technology platform for their core business. The rest still rely on a mix of email, spreadsheets, and itinerary builders.

As Arival CEO Douglas Quinby said in announcing the firm's 2025 multi-day research, "Operators who still rely on spreadsheets are the first to feel the friction as distribution channels demand real-time APIs and instant booking. Closing that tech gap is critical for growth."

The result is predictable: sales teams respond slower, finance has no real-time view of margin, marketing cannot personalize at scale, and leadership makes decisions on lagging data.

"The operators who treat us like a vendor talk about cost savings. The ones who treat us like a partner talk about revenue. That single difference - how they frame the investment internally - is usually the strongest predictor of whether they'll actually grow from the platform,” says Tracy Sharp, VP of Commercial at Kaptio.

The operators pulling ahead have reframed the question. They are no longer asking "What system do we need to replace?" They are asking "What kind of business are we trying to build, and what infrastructure makes that possible?"

The first question gets you a slightly better version of what you already have. The second one builds a growth engine.

The Four Capabilities That Turn Travel Tech Into a Growth Engine

Most platforms automate work. Few build commercial advantage. The systems creating real growth share four characteristics.

1. Connected data that turns insight into action

When booking data, CRM, product inventory, and finance live in separate environments, teams spend more time reconciling information than acting on it.

UK-based Travel Nation, a specialist in complex multi-destination FIT itineraries, knows this firsthand. Before consolidating onto a single platform, the sales team was operating across email, spreadsheets, standalone itinerary tools, and manual payment processes – and enquiry response times had stretched to three weeks.

After unifying itinerary building, CRM, payments, and back-office workflows into one system, response times dropped to near-instant, enquiry-to-booking conversion for repeat clients hit 66%, and annual turnover grew 10%.

The shift from reactive reporting to proactive growth management is the single highest-leverage move most operators can make.

2. Customer-centric journeys that improve conversion

Many legacy travel systems were built around the back office. The booking experience was an afterthought. However, Arival's 2025 multi-day tour research found that while 75% of bookings on major platforms are instantly confirmed, many small and mid-sized operators still rely on manual processes, which makes it difficult to meet the demands of real-time distribution channels.

The mechanism is simple: faster quoting, cleaner itineraries, fewer round-trips between the customer and a sales agent. Every additional day between inquiry and deposit costs you bookings to a competitor with a faster system.

3. Personalization that drives premium revenue

Experience travel naturally lends itself to personalization. The challenge has historically been scaling it.

Connected traveler profiles, centralized preferences, and flexible product configuration allow operators to personalize at volume without operational drag. And the commercial impact is direct: McKinsey has found that companies using personalization effectively realize a 10-to-20 percent uplift in revenue by optimizing each stage of the customer journey.

For a tour operator running $50M in annual bookings, that range translates to $5M–$10M of incremental revenue – a meaningful increase.

The point is not that personalization is "nice to have." It is one of the highest-yield levers available to a modern operator.

4. Modular infrastructure that supports new business models

The experience travel industry is no longer single-product. Operators are blending FIT, group, cruise, rail, wellness, and bespoke offerings under one brand. Distribution models are expanding. Partnerships matter more.

Rigid platforms cannot support that evolution. When an operator wants to launch a new product line or enter a new market, the cost of doing so on legacy infrastructure is measured in months and headcount. On modular, API-driven infrastructure, it is measured in weeks.

One of our customers launched a new river cruise product in 90 days using existing platform capabilities they already had access to. The alternative - a separate booking system and parallel ops team - would have taken 18 months and a six-figure investment.

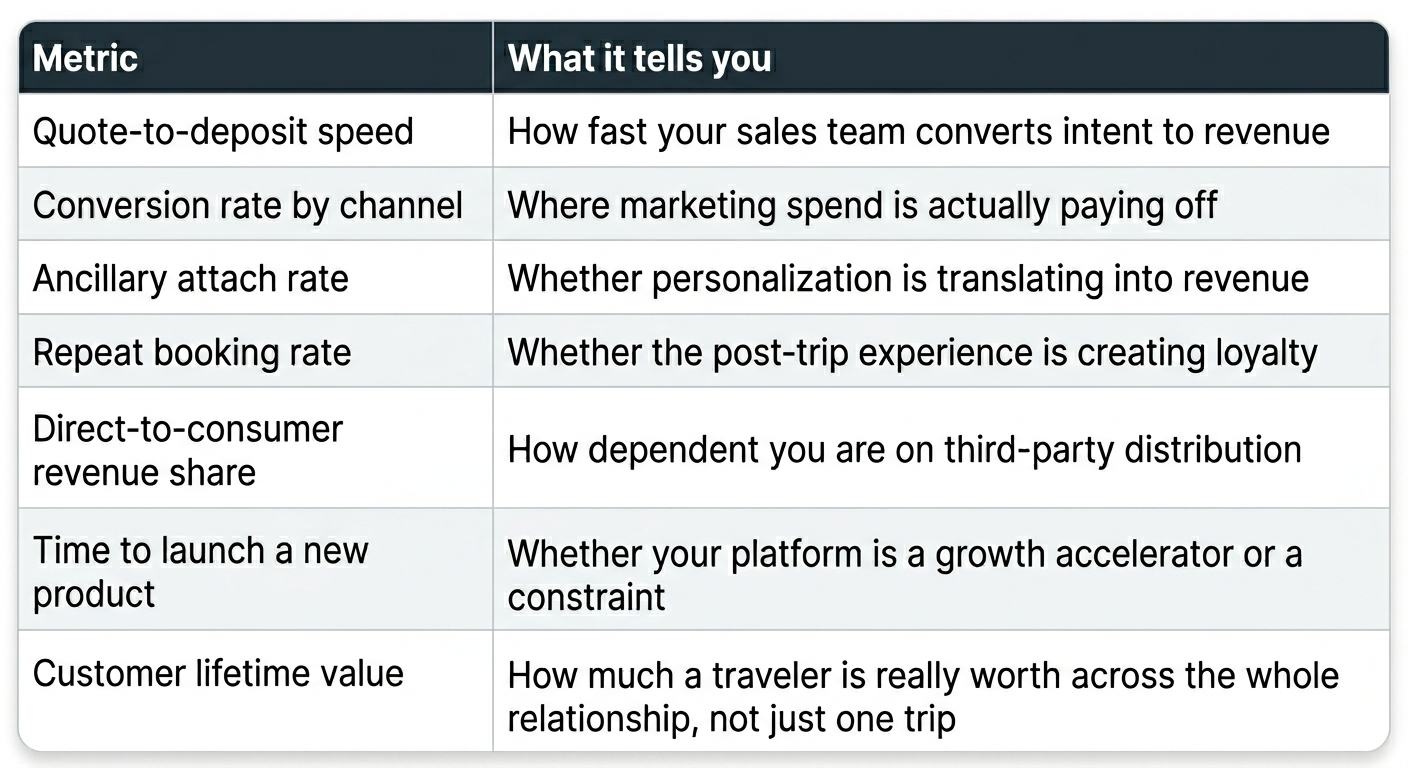

The KPIs That Actually Matter Now

One of the clearest signs of the industry shift is what operators have started measuring.

For most of the last decade, the dominant metrics were operational: hours saved, headcount avoided, time to close the books, number of itineraries processed per agent. Those numbers still matter - but they describe how well the back office is running, not how well the business is growing.

The operators treating technology as commercial infrastructure measure a different set of things: How much a traveler is really worth across the whole relationship, not just one trip.The shift from the first set of metrics to the second is subtle but important. The conversation moves from "How much time did we save?" to "How much growth did we unlock?"

One specific benchmark worth tracking: research on lead response time shows that inquiries responded to within one hour convert at 7x the rate of those waiting 24 hours or more.

For multi-day operators still managing quotes through email chains and spreadsheets, that gap is where bookings are being lost to OTAs, to faster competitors, or simply to traveler decision fatigue. Every day saved in the inquiry-to-quote window is measurable conversion lift. It is not an operational metric. It is a commercial one.

What the Operators Pulling Ahead Are Actually Doing

Three patterns show up consistently when you look at the multi-day operators outperforming their peers right now.

They have stopped trying to "buy a system" and started trying to build a stack. The best-performing operators are choosing modular infrastructure that connects to the rest of their commercial tools - payment providers, CRM, BI, marketing automation - and letting each tool do what it does best.

They are protecting human time, not eliminating it. Automation in this segment removes the manual work that prevents agents from doing the high-value parts of their job: Building relationships, designing trips, handling complex requests. The operators getting this right are reinvesting saved hours into customer experience.

They measure technology against revenue, not against cost. When the conversation about a platform investment is happening in operations alone, the bar is low. When it is happening in the C-suite alongside revenue targets, the bar - and the outcome - is different. The operators winning right now have moved the conversation upstairs.

The Mindset Shift That Matters Most

The operators leading the next decade of experience travel will not win because they have the most software. They will win because they treat technology as commercial infrastructure - measured in conversion, revenue per booking, and speed to market, not seats saved or hours reduced.

The brands building that infrastructure today are doing four things:

- Consolidating data so they can act on it, not just report on it

- Designing booking journeys around the customer, not the back office

- Using personalization as a revenue lever, not a service feature

- Choosing modular platforms that grow with the business, not against it

Automation got the industry this far. Growth is what comes next.

Kaptio works with multi-day operators building toward this model. See how we help operators move from automation to growth.

London, WC1N 2EB

Kópavogur, Iceland

Vancouver, BC, Canada, V6B 5C6